The delivery note is one of the goods accompanying documents and provides information about the goods contained in a shipment. It is either placed in the parcel by the sender (usually the manufacturer or retailer) or attached to the packaging, and serves as proof for the recipient of the goods received. The delivery note contains details of the delivered items, their quantity and unit.

Are you obliged to create a delivery note for your customers? The answer is no. And yet the delivery note is an important document for retailers and online shop operators in their business relationships.

There are neither legal requirements to issue delivery notes nor legally prescribed rules for their content and form. And yet almost all companies use the delivery note as a goods accompanying document, also known as a goods accompanying slip or goods accompanying letter.

What is a delivery note?

Definition and purpose

A delivery note is an informal but standardized document that lists exactly which goods or products were delivered, and in what quantity. However, it contains no prices and is not an invoice. With a delivery note, both the recipient and the sender can verify whether the delivered goods are complete and correct.

As a rule, the delivery note is a supplement to the invoice, but it is usually sent at the same time or even beforehand, especially in mail order business or for freight deliveries. In the event of a dispute, the delivery note serves as evidence that a delivery actually took place.

Whether a delivery note counts as an accounting document and is subject to special retention rules depends on its content. It is also crucial whether it only documents the delivery or also contains payment information.

Is your delivery note an accounting document?

Be careful when disposing of delivery notes! Even if there are no legal requirements to issue them, only delivery notes that do not constitute accounting documents may be disposed of. What exactly does that mean? In this context, please note the provisions of the German Fiscal Code (AO) Section 147 regarding the retention of documents:

- If it is a simple delivery note, it contains no payment details. With the information about the delivered goods and the order and delivery date, the simple delivery note is considered a business letter. Documents of this kind have a retention period of six years under Section 147 AO.

- If, in addition to the delivery details, the delivery note contains the request for payment, it is to be regarded as an invoice. In this case, it does not fall under the business letters pursuant to Section 147 AO. For invoices, a retention period of ten years applies.

As soon as the delivery note becomes an accounting document within business processes, retention periods of 6 or even 10 years apply.

Are there any mandatory details for delivery notes?

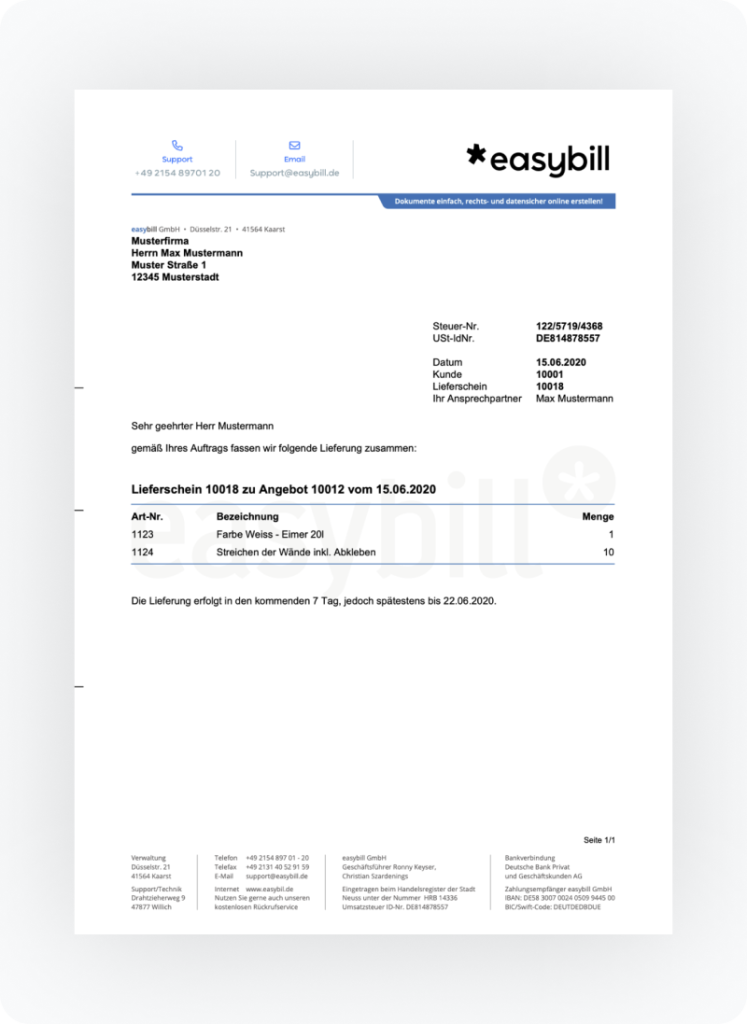

Although there are no mandatory details regarding the content of the delivery note, the following details, among others, have become established as standard in order to simplify business processes for both the sender and the recipient:

- Names of the supplier and the recipient

- Delivery address of the recipient

Order number/order name

Date of the order and delivery - Quantity and designation of the individual goods

- if applicable, weight or unit prices

- if applicable, composition and number of packages

- if applicable, details of commissions

- any subsequent deliveries

Frequently asked questions about the delivery note

When goods are delivered, it can be used to check the scope and type of the ordered goods and to ensure that the quantity, quality and type of goods delivered actually match what was ordered. In addition, it can help store the goods in the right place. The delivery note also offers the option of providing the recipient with additional information, such as technical data or special characteristics of the goods.

Here too, there are no legal requirements, but consecutive numbering has proven useful in day-to-day business as it provides greater transparency within accounting and document management. If the number of the corresponding invoice is also noted on the delivery note and vice versa, this offers significant simplification for both the sender and the recipient when matching up documents.

A delivery note can be issued both on paper and digitally. It is important that the document is clearly legible and traceable. In digital business transactions, electronic delivery notes are common, especially when using inventory management or invoicing systems. If the delivery note is archived digitally, the requirements of the GoBD (Principles for the Proper Keeping and Retention of Books, Records and Documents in Electronic Form) must be complied with.

A delivery note exclusively documents the delivery of goods, but does not contain a request for payment. The invoice, on the other hand, requests payment from the customer and must contain certain legally required information. If a price or payment term is stated on the delivery note, it may legally be considered an invoice—with corresponding tax implications. It is therefore advisable to clearly separate the functions of the two documents. Electronically generated delivery notes must be archived in accordance with the requirements of the GoBD. This means in particular:

● The documents must be stored in an unalterable form.

● It must be traceable when and how a delivery note was created.

● During a tax audit, the delivery note must be available at all times and machine-readable.

● Audit-proof archiving is ensured especially when using ERP systems or cloud-based delivery note creation (e.g. easybill).

For partial deliveries, the delivery note is used to clearly document the delivered part. It helps keep track of the status of an order—both for the customer and for the retailer. Ideally, the delivery note should indicate that it is a partial delivery and which items are still outstanding.

The GoBD apply to electronic delivery notes if the document is relevant for tax purposes or used as an accounting document. Specifically, this means: the document must be stored in an unalterable form. The time of creation must be traceable (e.g., through logging in the ERP system). Retention must be complete, proper, and machine-readable. Simple PDF filing is only sufficient if it meets the GoBD criteria and is audit-proof. If the delivery note is not used for accounting purposes, these requirements are less strict; nevertheless, consistent filing is recommended.

In the B2B sector, the delivery note primarily serves for goods receipt checks and internal documentation. In B2C retail, it is more commonly used to simplify returns and as an information document. It is not mandatory in either case.

Yes. In sensitive areas such as food, pharmaceuticals, mechanical engineering, or hazardous goods, additional details such as batch numbers, technical specifications, or safety instructions often have to be included. These arise from industry-specific requirements, not from general delivery note rules.

For partial deliveries, it should be clear that only part of the order was delivered and which line items are still outstanding. This makes allocation easier and prevents misunderstandings.

For international shipments, the delivery note supports export processing, supplements freight and customs documents, and helps to clearly verify the contents of the shipment. However, it does not replace a commercial invoice.

Prices may be stated, but this may, in case of doubt, turn the delivery note into an invoice. This would mean that the statutory requirements for invoices and the ten-year retention period would apply. For this reason, many companies omit price information.

A signature is not required. However, it can be useful if the handover is to be documented, for example for high-value or sensitive goods. In mail order, it is uncommon due to the carrier’s delivery documentation.