Differential Taxation

Differential taxation simply explained: What does it mean?

As an entrepreneur, you purchase durable goods on a commercial basis and resell them to your own customers. Under certain circumstances, so-called resellers can apply the margin scheme and thus benefit from it for tax purposes. You can read more about what exactly differential taxation is and what conditions apply here.

The term differential taxation means that resellers have to pay a lower sales tax on certain goods. In this case, the sales tax only applies to the difference between the purchase and sales price. Differential taxation is thus a special form of taxation for certain goods. The differential taxation is regulated in § 25a of the Value Added Tax Act (UStG).

According to this, the differential taxation applies to the supply of second-hand goods, such as antiques, collector’s items or works of art. However, differential taxation also applies to the trade in second-hand goods (used physical objects).

Differential taxation for resale

With the differential taxation one wants to avoid that for the object again the value added tax in full height becomes due. The full value of the VAT has already been paid when the goods were originally purchased. Therefore, with differential taxation, the sales tax is only applied to the difference between the purchase price and the resale price.

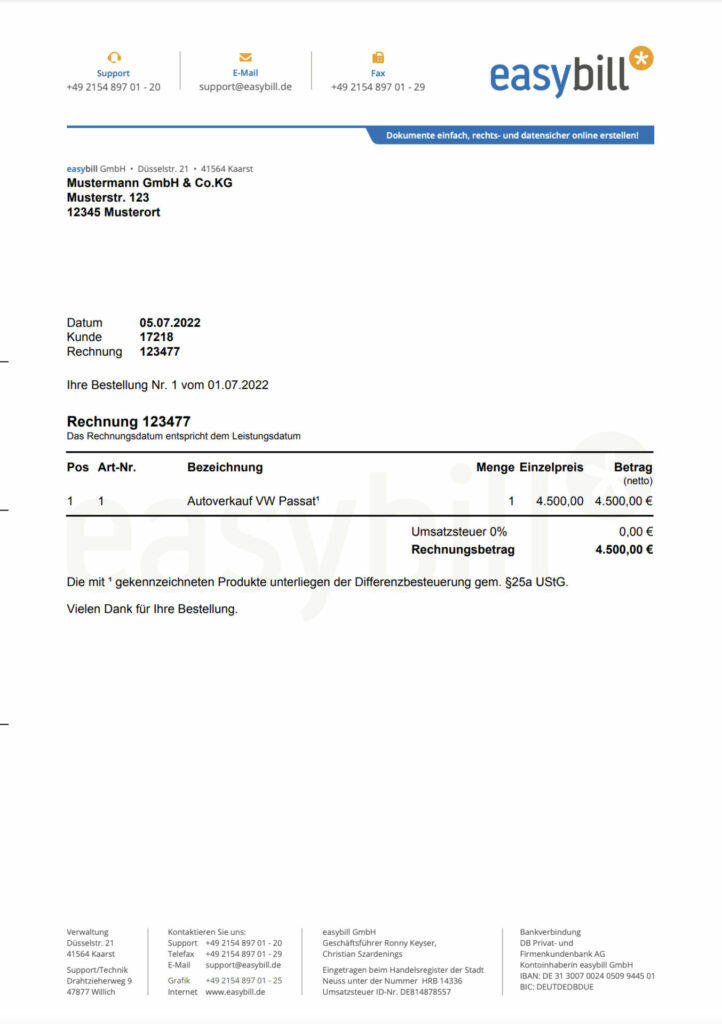

Differential taxation simply with easybill

Are you an online retailer and also sell items with differential taxation via a marketplace or your own online shop?

No problem for easybill!

The Import Manager recognizes your items with 0% tax and automatically shows the differential tax on the invoice. Save yourself the manual intervention or annoying subsequent corrections. Trust in your Invoicing software easybill.

The conditions of the differential taxation

As mentioned above, there are some requirements that must be met in order for sellers to even apply this type of taxation. These are:

- The goods must have been purchased in the Community territory, i.e. within the European Union.

- You, as the buyer, have not paid sales tax on the purchase of the commodity.

- You yourself as a reseller act commercially or publicly auction the purchased items.

Example of differential taxation

If the above conditions apply, the margin scheme can be applied. The following example explains the application in practice:

Let’s assume you buy a used car from a private individual in another EU country. The seller would like to receive 20,000 euros from you for the car. Since the seller is a private person, no input tax is due for the purchase. After a few weeks, you resell the car in Germany. You find a buyer who pays 25,000 euros for the car. Now the differential taxation comes into play. According to § 25a UStG, you only have to pay VAT on the difference between the purchase and sales price. In the concrete case this is

25.000 Euro – 20.000 Euro = 5.000 Euro

So instead of having to pay tax on the entire amount, only 5,000 euros are taxed. In this case, the sales tax amounts to 950 euros. For comparison: If the entire amount had been taxed, you would have had to pay 4,750 euros in sales tax.